Rental Income Tax Malaysia Public Ruling

Malaysia Taxation Junior Diary Investment Holding Charge Under 60f 60fa

.jpg)

Financing And Leases Tax Treatment Acca Global

Inland Revenue Board Of Malaysia Pdf Free Download

Lembaga Hasil Dalam Neger

Malaysia Taxation Junior Diary Investment Holding Charge Under 60f 60fa

2

.jpg)

A letting of real property as a business source under paragraph 4 a of the income tax act 1967 ita.

Rental income tax malaysia public ruling. Such rental income is explained under section 4 d of the act. Rental income is. In malaysia income derived from letting of real properties is taxable under paragraph 4 a business income or 4 d rental income of the income tax act 1967. Director general s public ruling section 138a of the income tax act 1967 ita provides that the director general is empowered to make a public ruling in relation to the application of any provisions of the ita.

Individuals who own property situated in malaysia and receive rental income in return are subject to income tax. 19 december 2018 1. Objective this public ruling pr explains. Deloitte tax hand information and insights from deloitte s tax specialists globally.

And b letting of real property as a non business source under paragraph 4 d of the ita. The income is deemed as a business sources if maintenance services or support services are comprehensively and actively provided in relation to the real property. A public ruling as provided for under section 138a of the income tax act 1967 is issued for the purpose of providing guidance for the public and officers of the inland revenue board malaysia.

Five Public Rulings Updated And One New Public Ruling Issued By The Inland Revenue Board Ey Malaysia

Financing And Leases Tax Treatment Acca Global

Withholding Tax 101 Legally Malaysians

Http Lampiran1 Hasil Gov My Pdf Pdfam Pr5 2017 Pdf

Inland Revenue Board Malaysia Interest Expense And Interest Restriction Pdf Free Download

8 Things To Know When Declaring Rental Income To Lhdn

Inland Revenue Board Of Malaysia Pdf Free Download

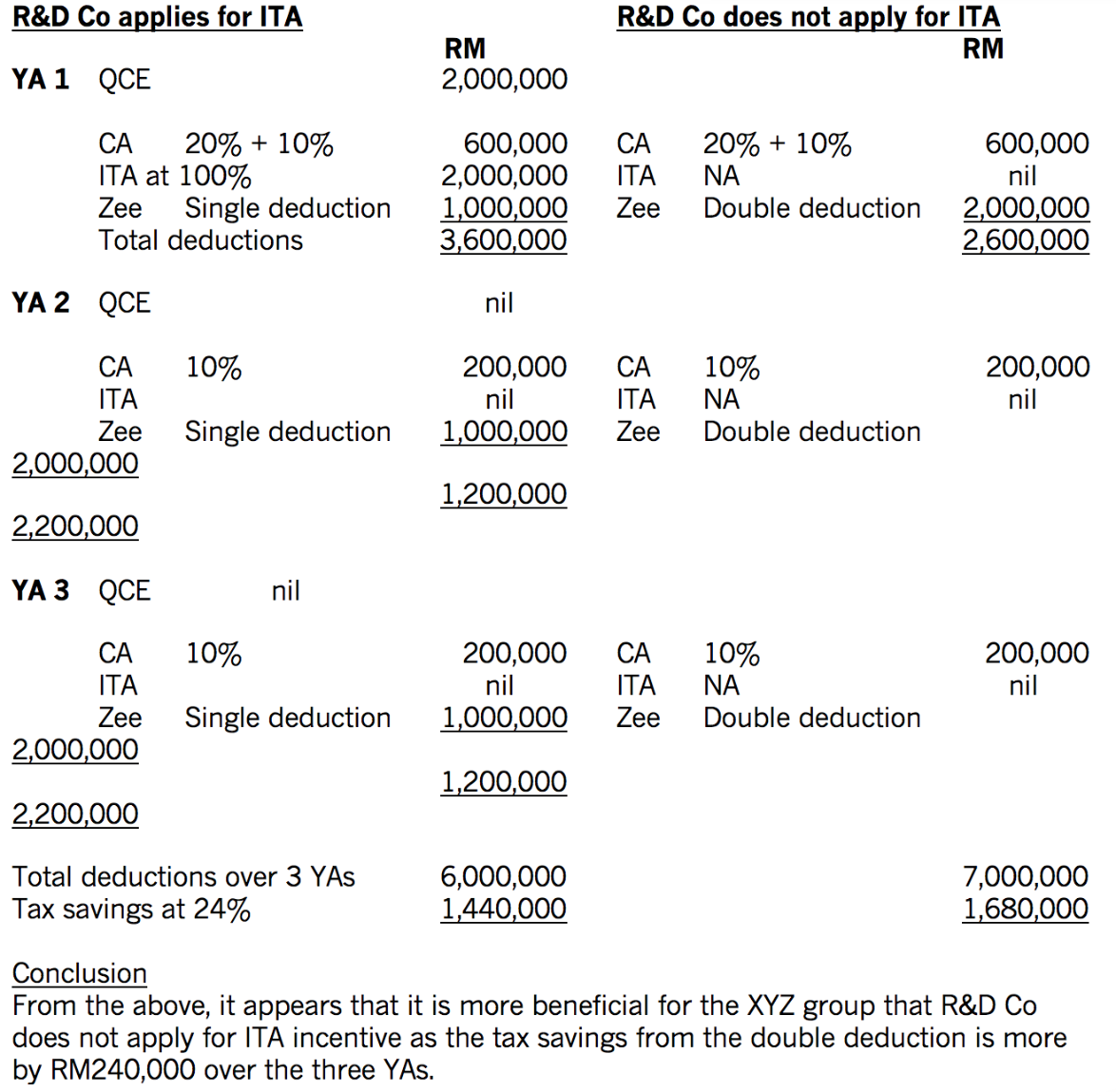

Tax Incentives For Research And Development In Malaysia Acca Global

Http Lampiran2 Hasil Gov My Pdf Pdfam Pr 11 2019 Pdf

Inland Revenue Board Of Malaysia Investment Holding Company Public Ruling No Course Hero

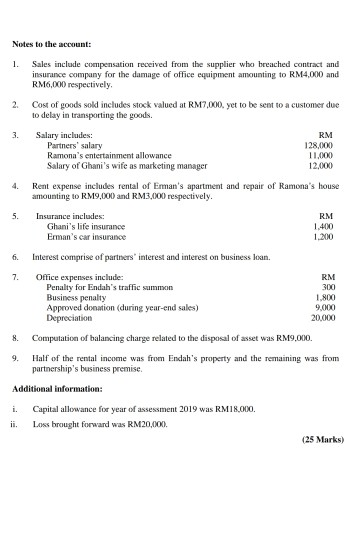

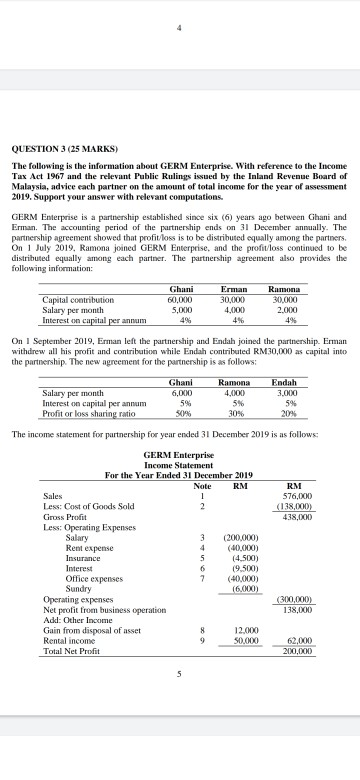

Question 3 25 Marks The Following Is The Informa Chegg Com

Note 4 Taxation For Specialised Industry 1 Double Taxation Taxation In The United States

Question 3 25 Marks The Following Is The Informa Chegg Com

.jpg)